This article was paid for by a contributing third party.

Embracing the next evolution of FX swaps

Gavin Wells, head of swaps strategy at 360T, explores new products and growth drivers in the FX swaps market, and explains how MidMatch – the firm’s fully automated FX swaps limit order book with mid-rate matching capability – can help clients capitalise on them

New products coming to the FX swaps market suggest an evolution is at hand. Before considering how that might occur, it helps to understand what is driving the continued growth in this, the largest product segment of the FX market.

Over the past decade there has been a shift in the types and numbers of market participants using FX swaps and their reasons for doing so. As the market is largely opaque, much of this went unnoticed until you see the common thread running through a number of articles in the press over the past 18 months.

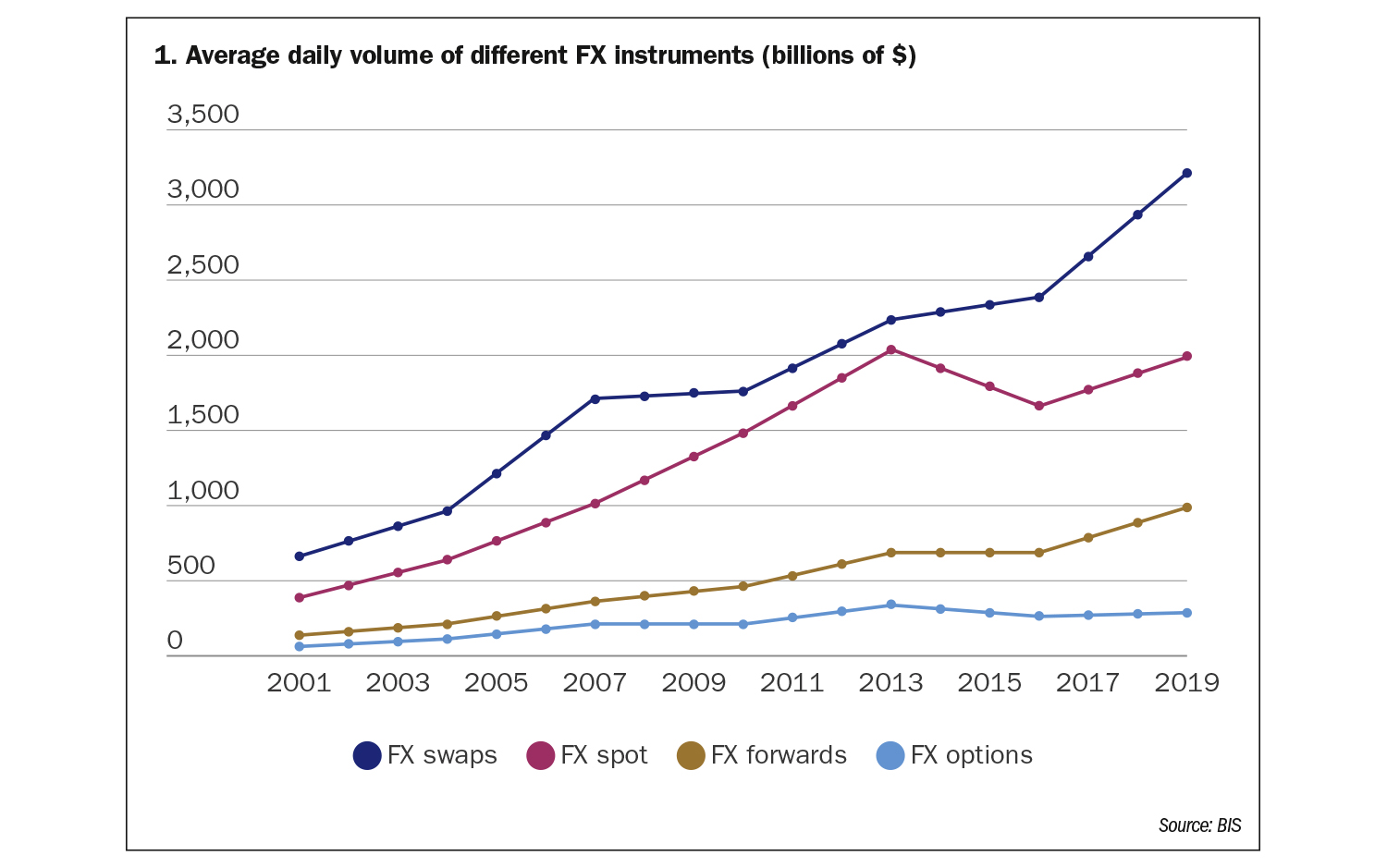

The first of these was the Bank for International Settlements’ (BIS’) last triennial survey of the FX market, which took place in 2019, and revealed that the daily turnover of FX swaps trading rose 34.7% over the preceding three years to $3.2 trillion in notional value.

When you consider this growth in notional terms – an extra $825 billion of FX swaps traded each day – and contrast this to spot, forwards and options, which grew by $335 billion, $300 billion and $43 billion, respectively, it becomes clear the FX swaps growth was out of sync with the broader trend in the FX industry (see figure 1). This suggests there are growth drivers specific to FX swaps – but what are they?

New market participants

Across financial markets, increased capital and collateral requirements have increased funding needs. While FX market participants have used FX swaps to hedge, roll and fund their FX positions, outside FX this funding has historically come more from repo and money markets and, in times of stress, from the swap lines offered by some central banks since the crisis that began in 2007–08.

This has now changed: “global finance is increasingly dependent on opaque currency trading to keep cash flowing”, bringing new participants to the FX market. This view is supported by reports that the renewal of central bank swap lines may not be needed, as “the FX swaps market can meet those funding needs”. Add to this potential capital savings on FX swaps from new models such as the standardised approach for measuring counterparty credit risk, and the product is not only meeting a need but becoming more cost-effective in doing so.

Accepting that FX swaps are now recognised and wanted as a reliable product for funding explains their increased growth through a larger user base. In the absence of other developments, this suggests the smart money is on next year’s BIS survey finding the growth trend continuing. What does this mean for the previously suggested evolution?

In the limelight

When new participants enter a market, fuelling its growth, existing processes and platforms naturally come under scrutiny. Through this it has become apparent that traditional infrastructure for trading FX swaps is no longer adequate for a market that is now so big, widely utilised and increasingly important to the wider financial markets’ ecosystem.

Applying lessons from other markets, brought by new participants, there is now a big push to provide trading infrastructure that is stronger, more resilient and more efficient to cope with this increased demand. One leading market publication noted: “With no central limit order book and little publicly available data, FX swaps market structure will likely be a key theme for the next few years.”

Heeding market and client commentary, and considering many of the innovations implemented in the spot market in the 2000s around e-trading, automated hedging and credit models, 360T decided to meet market needs by developing a fully automated FX swaps limit order book with mid-rate matching capability – known as MidMatch.

A better way to trade

MidMatch supports graphical user interface (GUI) and application programming interface (API) trading with a choice of automated credit solutions. It uses 360T’s award-winning Swaps Data Feed as a reference for grey-book risk exchange at mid-market. It is built on the same technology that runs our already robust and low-latency spot products.

The FX swaps market will benefit from this improved price transparency and more robust trading ecosystem and infrastructure. MidMatch will support market growth, further enhancing liquidity and the use of FX swaps as a source of funding for the global financial system.

Crucially, it also has quantifiable economic benefits for the traditional participants in this marketplace. It creates the opportunity to build out a new revenue line in auto-trading swaps and enhancing existing algo execution suites to include these; the potential to exchange risk at mid-market offers a reduction in the spread paid by traders; and, as we’ve witnessed across multiple asset classes, automated trading helps reduce operational costs and inefficiencies.

Improving productivity

Shifting to a new model of trading often raises questions from existing market participants, and typically these have centred around the automated credit component. Though this is often an initial source of concern in our discussions, we – and our bank partners who are already live on the MidMatch platform – have implemented solutions that are strikingly simple.

One option is to integrate the user’s proprietary credit engine with MidMatch through a financial information exchange API, providing real-time credit updates; the other is to use our Limit Monitor, which enables users to create granular, parameterised rules to assign credit lines and choose from six different risk methodologies to define how these are utilised. These credit models are necessary to support automated trading and remove time-consuming and error-prone manual credit checks still much used for GUI trading.

The other question occasionally raised during conversations about FX swaps market evolution is what this all means for the human trader. This is not unique to FX swaps. As a technology company we hear this asked frequently by a wide range of clients across product segments and geographies. The answer is nearly always the same: this technology is not designed to replace humans but rather to enhance and augment their abilities.

FX swaps traders have expertise and a skill set that cannot be replicated. Automated trading solutions offer a means for them to deploy these in a more effective and productive manner. We are clear that, no matter how sophisticated the technology becomes, there needs to be a trader in the cockpit to direct it.

Embracing change

It is very likely the evolution of FX swaps as a source of funding will continue to drive growth in this product segment, which will maintain pressure to implement better infrastructure models. If there are lessons to learn from similar technological changes that occurred in the FX spot market many years ago, it’s that the price of continually doing the same thing can be far higher than the price of change.

Many firms recognise this and are now either live participants on MidMatch or in the process of onboarding.

Sponsored content

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@fx-markets.com

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@fx-markets.com